Twice the Maternal love, but Twice the Inheritance Tax Burden

The Utley family have shared in the national press their heart-warming story of sisterly devotion, and their worries about the way a wholly unexpected turn of events has placed them in a dilemma they’re unsure how to solve. Here are some potential solutions.

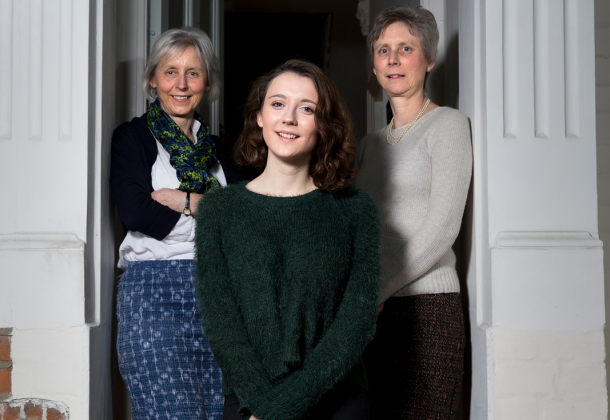

Livvy Utley was a surprise blessing to her mother Catherine back in 1993. Catherine was single and knew that she would be bringing Livvy up alone, but her devoted sister Ginda was with her every step of the way, and together they raised Livvy in a happy family of unit three. Livvy always regarded herself as having two Mums, rather than a Mum and an Aunt. Ginda played as important a role in the day to day business of bringing up Livvy as Catherine did.

An unexpected windfall – and a heavy inheritance tax burden

Catherine and Ginda bought a little house together in Battersea, London, when Livvy was small. That house has been their family home ever since. And now that Livvy has graduated from university, she is back home, living full time with her two Mums. Catherine and Ginda are in their 50’s now, and their thoughts have turned towards later life, and, crucially, making sure Livvy always has her home, even when one or both of them has passed away.

The extent of the boom in property values in London could not have been predicted back in the mid-nineties. Ginda and Catherine would never have believed it, when they moved in, if someone had told them to expect their modest terraced home to be worth £800,000 to £950,000 by 2016.

And this is where their problem lies. If Catherine or Ginda were to die, a crippling inheritance tax would have to be paid within six months. On 2016 figures, the tax liability would be £30,000 to £60,000. And that liability only going to increase year on year as London property values continue to soar.

For the Utley family, the death of one of the sisters would mean their house having to be sold to raise the money to pay the inheritance tax bill. The prospect of losing one third of their family, shortly followed by the loss of their family home, is bleak in the extreme.

A “proper family”.

The family understandably feel that the law is unfair to them, because it doesn’t recognise them as a “proper” family. Married couples and couples in civil partnerships can inherit from each other without incurring Inheritance Tax, and their tax-free allowances - their “Nil Rate Bands” - can be transferred between them.

If Ginda and Catherine had been best friends raising Livvy together, they could have entered into a civil partnership – there is no legal requirement for a sexual relationship between civil partners. But as sisters, civil partnership is not an option that is open to them.

If Ginda had adopted Livvy when she was a child, the impact could have been alleviated to some extent. The new enhanced Nil Rate Band, which comes fully into force in 2020, enables a “direct descendant”, including an adopted child, to inherit a share in the main family home up to the value of £500,000 without any inheritance tax liability. So, both Ginda and Catherine would, by 2020, have been able to use this provision to allow Livvy to inherit at a much reduced, or even fully eliminated, tax burden. But sadly, adult adoption isn’t available in the UK, having been specifically ruled out by the Adoption and Children Act 2002. So, the enhanced Nil Rate Band will only be available to Catherine and not to Ginda.

The Utley sisters are skilfully lobbying MP’s and are hoping that a Bill will be tabled in parliament which, if passed, will enable long-term cohabiting siblings to be treated the same as married couples and civil partners for inheritance tax purposes.

Two possible solutions.

Meanwhile, is there anything the Utley family can do right now to mitigate the burden?

Catherine and Ginda could each gift a share of their house to Livvy, so that the house is co-owned by the three of them. Provided that Livvy remains permanently living at the house, and provided Catherine and Ginda do not receive a “collateral benefit”, such as Livvy taking over responsibility for all the household bills, a gift of that kind would be “potentially exempt” from inheritance tax – i.e. no inheritance tax would be paid if Ginda and/or Catherine lived for at least seven years after the gift was given.

The downside of this is that it limits Livvy’s life choices. If, for example, Livvy got married and moved to another home with her spouse, the “potentially exempt” gift would immediately become a “gift with reservation”, and the inheritance tax advantage would be lost. The key to this kind of gift being effective for inheritance tax purposes is for Livvy to have “bona fide possession and enjoyment”, by living at the house.

An alternative approach would be to use life insurance. Ginda and Catherine could each take out a life insurance policy in amounts sufficient to pay the tax bills on their deaths. The cost of life insurance is at a historic low, and a life policy for £100,000 for a single non-smoking woman in her fifties can cost as little as £40 a month.

For this approach to work for Catherine and Ginda, they would need to bear two important things in mind. First, it’s essential that the policy is “written in trust” for the executors of their wills. That way, on their death, the policy’s proceeds go to their executors to pay the inheritance tax, without forming part of their assets. If their estate assets included the policy proceeds, that would only swell the tax bill.

Second, it would be a good idea to review things every few years to make sure they each have enough cover the pay the eventual tax bill. As the value of their house rises, so potentially would their inheritance tax liability, which might mean they would need more life cover.

At WillWritten, we believe every family is a proper family, and our mission is to empower all families to have their assets protected and their wishes respected. Proper estate planning puts you – not the politicians – in control. So if you’d like to find out more about protecting the interests of your family, feel free to get in touch, either by completing the contact form below, or by calling us on 0151 601 5399.

-

The Probate Process Demystified

Probate, a term that often appears daunting, is the process of putting someone's affairs in order after they've passed away.

Read more... -

Navigating Inheritance Tax

Let’s explore some valuable insights and tips to help you navigate Inheritance Tax effectively.

Read more... -

Peace of Mind for Parents of Young Children

As a parent, your primary concern is the well-being of your children. You strive to provide them with love, care, and a secure environment to grow and thrive. Yet, amid the joyful chaos of parenting, it's easy to overlook one crucial aspect of their future: creating a Will.

Read more... -

Safeguarding Your Business Legacy

Let’s explore four key strategies that every business owner should consider safeguarding their business legacy.

Read more... -

The Essential Guide to Estate Planning for Private Landlords

The rewards of property investing can be generous, but the challenges are undeniable. Let's look at the bigger picture.

Read more... -

Blended Families and Inheritance: Balancing Your Spouse’s Security and Your Children’s Legacy

Being part of a blended family can be such a joy and can also raise important considerations for the future.

Read more...

-

Protecting Your Children’s Inheritance from Care Costs

Life is full of uncertainties, and as responsible parents and grandparents, it's only natural to worry about what the future holds for your loved ones.

Read more... -

A Guest Blog from Canada

Brian from Canada tells his story of the difficulties he had with his late father's estate due to poor estate planning. It shows that the risks - and the ways to prevent them - are remarkably similar on both sides of the Atlantic.

Read more... -

Vlog: Powers of Attorney Explained

A simple video introduction to Powers of Attorney, what they do for you and what your rights and your Attorney's responsibilities are.

Read more... -

Vlog: How to Divorce-Proof your Children’s Inheritance

A simple video tutorial addressing a concern held by many parents of adult children.

Read more... -

Take me to Court (as your barrister of course!)

Barrister Raj Kanda tells us how a revolution in legal services means you can access his help directly.

Read more... -

Why Trusts are your Best Friend

A short video blog explaining why trusts are a user-friendly and economical part of your overall estate plan

Read more... -

Shielding your Buy to Let Portfolio from Inheritance Tax

This is a quick video introduction to seven ideas you can explore to manage your exposure to Inheritance Tax if you're a buy-to let investor

Read more... -

Estate Planning Video Tutorial for Buy to Let Investors

This short video introduces you to the main points you need to consider if you are responsible for a buy to let portfolio

Read more... -

Video Blog - How to Protect your House from Care Fees

This is the biggest issue for more mature parents whose kids have flown the nest - how can we save the kids' inheritance from being wiped out by care fees?

Read more... -

Video Blog: How to Pay for a Funeral Without Going Into Debt

It's a terrible time when you've just been bereaved, and the last thing you need is practical worries about paying for the funeral.

Read more... -

A Scary Story! Video Blog

My video explaining how a simple keystroke error almost cost someone their £100k+ inheritance … and what easy action you can take to safeguard yourself against such a thing happening to you.

Read more... -

Older Childless People “Dangerously Unsupported”

More than a million childless people aged 65 or above are living with dangerously inadequate levels of support, suffering isolation and lack of access to formal care - and that number is expected to double by 2030.

Read more... -

Taking the Long View

You need to make an estate plan to truly future-proof your family. Here's why, and how to go about it.

Read more... -

Brexit Turmoil Delivers Reprieve for Bereaved Families

At last, a tiny bright spot amongst the relentless Brexit related misery.

Read more... -

£110,000 for seven years of care

A court has awarded £110,000 to a granddaughter who provided devoted live-in care for her grandmother for seven years.

Read more... -

What to Do When a Loved One Passes Away

When you lose someone, the last thing you want is to think about the practicalities, but there are some essential steps you must take to safeguard the estate and ensure that it is passed down as smoothly as possible.

Read more... -

Estate Planning Essentials for Same-Sex Couples

How to avoid the four most common estate planning pitfalls that can affect same-sex couples.

Read more... -

D’Oh! Five Ways to Seriously Mess Up Your Estate Plan

If financial security and peace of mind for your nearest and dearest is your priority, it’s essential that you maintain a valid and up to date estate plan.

Read more... -

Talking About Estate Planning with your Parents

Have your Mum & Dad made their estate plan yet? Should you be concerned?

Read more... -

What About Your Digital legacy?

How to plan for what will happen to all your online accounts after you’ve gone.

Read more... -

Don’t let your business get clobbered!

It’s your responsibility to safeguard your business. Here’s how to do it in three easy steps.

Read more... -

Cost of Care Rises by 10% in Just One Year

The cost of a place in a care home is rising at its fastest rate ever, while pension incomes have little hope of keeping pace.

Read more... -

Hats off to the “Parentsioners”!

Look around, and you’ll notice you're surrounded by people who quietly go about their daily business of achieving seemingly impossible feats of hard work and organisation. You might be looking at just such a person in the mirror.

Read more... -

Contested Will Saga Ends in Prison Sentence

A retired window cleaner, who was left £280,000 in the will of a customer, was jailed for failing to hand back the money when ordered.

Read more... -

Will Inheritance Tax be Simplified?

The Office for Tax Simplification is reviewing the complex Inheritance Tax system. Does this mean there will there be less tax to pay?

Read more... -

Daughters try to block father’s marriage

Court of Protection forced to decide whether daughters can lawfully block their father’s marriage to his partner of 20 years.

Read more... -

Three Brothers in Court Battle Over their Mother’s Legacy

The three Heath brothers have already incurred £50,000 in court costs because they didn't have the awkward family conversation about inheritance.

Read more... -

We Need to Talk About Inheritance

With inherited wealth set to double in the next 20 years, it’s time to get over the awkwardness and have the conversation now.

Read more... -

Inheritance Tax Bonanza for HMRC

A 23% spike in Inheritance Tax receipts is being blamed on frozen allowances, rising house prices and more aggressive tax collection.

Read more... -

Dementia Tax – Some Good News?

Cautious optimism as Health Secretary vows to bring forward plans to make paying for care fairer.

Read more... -

The Tragic Case of “Mr Y”

52-year-old "Mr Y" is being kept alive in a coma while the Official Solicitor defends legal principles.

Read more... -

Can the Government be Trusted on the Dementia Tax?

Little has been said about the cost of care since the 2017 Dementia Tax controversy. But the few hints dropped by the government have both insulted and threatened parents of adult children.

Read more... -

Power of Attorney Refunds Available

If you paid £110 to register your Lasting Power of Attorney between 1st April 2013 and 31st March 2017, you are entitled to a refund of up to £54.

Read more... -

Case Study: Jim and Jean’s Story

Jim and Jean have two grown-up children with complex disabilities. Here’s how their estate plan met their needs.

Read more... -

The £50million Final Salary Pension Transfer Boom

Here’s why so many savers are moving away from their final salary pension schemes? And why your pension capital should be a key consideration in your estate plan.

Read more... -

Just how risky are Lasting Powers of Attorney?

An invaluable tool? Or a passport to financial abuse?

Read more... -

Case Study: Guy and Steve Safeguard their Business

Read more... -

Sheila Kitzinger’s Good Death

Sheila Kitzinger, a passionate advocate for the rights of expectant mothers, pioneered the use of birth plans. And she brought the same control and empowerment to planning her own final days.

Read more... -

We’re Not Getting Any Older

Life expectancy at age 64 has all but ground to halt, due to the austerity years and a surge in dementia. What can you do for yourself while we wait for a cure?

Read more... -

Lynda Bellingham’s Sons Betrayed, as Feared

The late Lynda Bellingham’s lack of a proper estate plan risked leaving her sons with nothing – now her widower has done exactly what she least wanted him to do.

Read more... -

Probate: What’s it all about?

If you are dealing for the first time with the estate of someone who has died, you must quickly get to grips with some probably unfamiliar concepts. This is a short introduction to the issues you may have to deal with.

Read more... -

Redefining old age?

Seismic demographic changes mean we must re-think what it means to be “old”, says one of the UK’s leading social scientists.

Read more... -

Case Study: Ray & Joyce

How this retired couple made sure most of their main asset would be inherited by their children – and not the council.

Read more... -

Business Property Relief

If you are a business owner, it’s likely that your business is one of your main assets. You may want to pass your business to the next generation as a going concern, or you may want your dependants to benefit from the value of the business after you’ve gone.

Read more... -

Seven Inheritance Tax Tips for Buy to Let Investors

If you’ve invested in buy-to-let, you’ve probably done so with the intention of creating a steady income for yourself, together with capital to hand on to the next generation when you’re gone. But unfortunately, wealth tied up in residential lettings often comes with a significant Inheritance Tax burden.

Read more... -

The Residence Nil Rate Band

A guide to making the most of the new Inheritance Tax allowance.

Read more... -

Case Study: Tony and Diane’s Story

How Tony and Diane secured an Inheritance-Tax-free legacy for their daughter and planned a secure retirement for themselves.

Read more... -

What’s all this fuss about The Dementia Tax?

It’s odd that there has been so much vociferous debate about “the dementia tax”, as if this is an outrageous new concept proposed by a rapacious government. The truth is that people with dementia have been robbed of their legacy for decades to pay for their care.

Read more... -

Separating Elderly Couples in Care is Inhumane

It's scary that Social Care leaders actually had to be told at a recent conference that separating elderly couples in care is inhumane.

Read more... -

Inheritance Tax Planning with Enterprise Investment Schemes

Not keen on the government gate-crashing your funeral to demand yet more tax? An Enterprise Investment Scheme may be a useful addition to your estate planning toolkit.

Read more... -

Sons’ Inheritance Blown on Legal Fees

Two brothers have wasted their entire inheritance on a doomed court battle to contest their late father’s will.

Read more... -

Helping your Parents to Cope

The Guardian newspaper recently published a helpful group discussion, in which readers shared their own experiences of what has worked for them in offering a helping hand when a parent is finding it all too much.

Read more... -

The Supreme Court’s Decision in Heather Ilott’s case.

The 2015 Court of Appeal Decision in Heather Ilott’s case has been overturned. The Court of Appeal’s 2015 award of £163,000 has been reduced to £50,000.

Read more... -

Charitable Legacies - a Win-Win

Leaving a charitable legacy in your Will makes you feel good AND gets you an Inheritance Tax discount – what’s not to love?

Read more... -

Our friend died without saying she’d left us £110k

The rate at which estates go unclaimed has risen two and a half times in the last five years, according to government figures recently released.

Read more... -

Who gets the kids if something happens to us?

It’s a horrible thought, isn’t it? Nobody wants to imagine their beloved child being orphaned, but thinking about the unthinkable, and making proper plans, is a vital parental responsibility.

Read more... -

Is Your Child’s Inheritance Divorce-Proof?

Doreen Crowther may lose her house because her inheritance wasn't divorce-proofed.

Read more... -

Planning for the Cost of Care

Will poor health in later life put your home at risk?

Read more... -

Status Quo Rocker Rick Parfitt Disinherited his Wife

The late Status Quo star Rick Parfitt disinherited his wife in the final days before he died, it has emerged. But all is not as it seems.

Read more... -

My Health Scare - and why I’m so glad I made an Estate Plan

My New Year was overshadowed by a major health scare – but my estate plan assured me that, whatever might happen, my clients and loved ones are protected

Read more... -

Your New Year’s Resolution?

If you haven't made your will yet, you risk leaving a mess behind for the people you love.

Read more... -

George Michael’s Estate Plan

Much missed pop legend provides for his sisters, god-children and favourite charities in his Will

Read more... -

Our 2017 Continuing Professional Development Programme

Our 2017 Estate Planning Training Programme for Accountants and Financial Services Professionals

Read more... -

How a £2000 Inheritance Transformed 40,000 lives

Vashti Seth started a charity with a legacy from her dad

Read more... -

The £72million House Heist

Councils’ £72million raid on older people’s houses to pay for care

Read more... -

Royle Family’s Caroline Aherne Accidentally Left Her Mum with a £71,000 Inheritance Tax Bill

Inheritance Tax stress for Caroline Aherne's bereaved Mum

Read more... -

“Get a Job!”: Disinherited Daughter’s Court Battle Ends in Humiliation

Danielle Ames loses her fight with her stepmother for a share in her late father’s fortune

Read more... -

Danae Brook’s Story: A Blended Family Blighted by Intestacy

How Danae’s husband’s intestacy left this blended family in chaos.

Read more... -

The Truth about Deliberate Deprivation of Capital

Thinking about making a significant gift to your children? Worried that the council might snatch back the gift if you later go into a care home? Here’s what you need to know.

Read more... -

Disinherited Daughter v Stepmother

Disinherited Danielle Ames in Court Battle with her Stepmother over her "Idolised" Late Father's Fortune

Read more... -

Is the Traditional Marriage an Endangered Species?

In a major cultural shift, married couples are now in the minority as most couples choose to cohabit. Is this the beginning of the end for traditional marriage?

Read more... -

Video Blog - Inheritance Tax and You

Will my estate be affected by Inheritance Tax?

Read more... -

The Hurt and Rejection of Daisy Goodwin

It's every parent's responsibility to talk to their children about the legacy they might leave

Read more... -

Trusts to Manage Inheritance Tax – One Rule for The Duke of Westminster and One for the Rest of Us?

The toxic urban myth that Inheritance Tax is for "the little people".

Read more... -

Toby Wales’s Story

The power of wills to transform lives for the better.

Read more... -

Heartache and Chaos from a Lost Will

Alison Shields tells of the distressing consequences of her father's lost will.

Read more... -

Father’s fear of making a will left his young daughter penniless

How Katy Young was accidentally disinherited by her father's fear of making a will.

Read more... -

Property tycoon sued beyond the grave.

Ex-civil partner of deceased millionairess in court bid for larger settlement

Read more... -

Stepfamilies & Blended Families Estate and Legacy Planning

A video guide for people who have stepfamilies or blended families

Read more... -

Frugal Bachelor Leaves Surprise Legacy of £1.5million to his Local Hospital

Heartwarming Generosity of Peter Gibbons

Read more... -

Case Study - How Dervla’s Inheritance Tax Planning Saved £120k

In today’s climate, “fail to plan” means “plan to pay lots of Inheritance Tax”

Read more... -

Video Blog - Estate Planning Tips for Business Owners

A Video Guide to Keeping your Business Resilient

Read more... -

Angela Rippon – a Happy Singleton Putting her Affairs in Order

In advance of the BBC documentary "The Truth About Dementia", Angela Rippon shares her concerns.

Read more... -

“Do Not Resuscitate” – Could this Happen to You Without your Consent?

The NHS knows that it's happening - and why it's happening - but won't be doing anything about it anytime soon. Here's how to protect yourself and your family.

Read more... -

The 8 Vital Questions You Should Answer Before You Make a Will or Estate Plan

How to choose an estate plan that's fit for purpose and within your budget

Read more... -

Estate Planning Tips for Happy Singletons

This is an estate planning guide for single people - what you, as a happy singleton, can do to plan a secure future and a meaningful legacy.

Read more... -

Oxo Mum’s Family Torn Asunder by a Badly Made Will

How poor estate planning has left the late Loose Women star’s sons powerless – and possibly penniless.

Read more... -

Case Study - Bill and Anne, Buy to Let Investors

How we helped a couple ensure a secure future for theselves, their family and their buy to let portfolio

Read more... -

Estate Planning Considerations for Buy to Let Investors

This is the first in a two-part series that looks at the estate planning concerns of buy to let investors - and some of the many available solutions.

Read more... -

Come Live with Me and Be my Love ....

Five practical tips for living together securely

Read more... -

Colin and Eleanor’s Story - Peace of Mind for Four Generations

This is the story of Colin and Eleanor, great-grandparents who wanted the peace of mind of knowing their assets were protected for the four generations of their family, and that their own personal wishes were respected no matter what

Read more... -

Soaring Probate Fees - a Stealth Tax

The Ministry of Justice has announced a fee scale that increases the cost of probate by up to 130 times the present fee. Here are some ways of managing the cost of leaving a legacy for your family, so their inheritance is maximised.

Read more...

Subscribe for Updates & Information

"I decided to get advice about making my will because I was about to travel abroad with my children for the first time in many years. My financial advisor recommended Will Written. I appreciated being able to have a consultation at home, so that I could discuss my situation in confidence. I was able to ask wide-ranging questions and Gina’s knowledge and expertise were reassuring. An estate plan was created for me that exactly suited my needs, resources, family and dependents. I have the peace of mind of having made a will that ensures my assets are safely passed to my children at the end of my life. I also have added protection if I become ill or disabled, because I have made a Lasting Power of Attorney appointing my best friend to manage my affairs if I lose the ability to manage them for myself. "

Christine J